Updated: February 2026

How to Maximize Your 2026 Business Vehicle Write-Offs Under Section 179

Section 179 allows businesses to deduct all or part of a qualifying vehicle’s cost in the year it’s placed in service, instead of spreading the deduction over multiple years. The amount you can deduct depends on the vehicle type, GVWR (gross vehicle weight rating), and your business-use percentage—so the first step is identifying which vehicle category you’re in (by GVWR and design) and confirming business-use percentage.

By leveraging Section 179, business owners can maximize first-year write-offs while keeping operations efficient.

Key takeaways for 2026:

- Business use must be more than 50% in the year the vehicle is placed in service.

- The overall Section 179 dollar limit and phase-out apply to your total qualifying property placed in service (including vehicles).

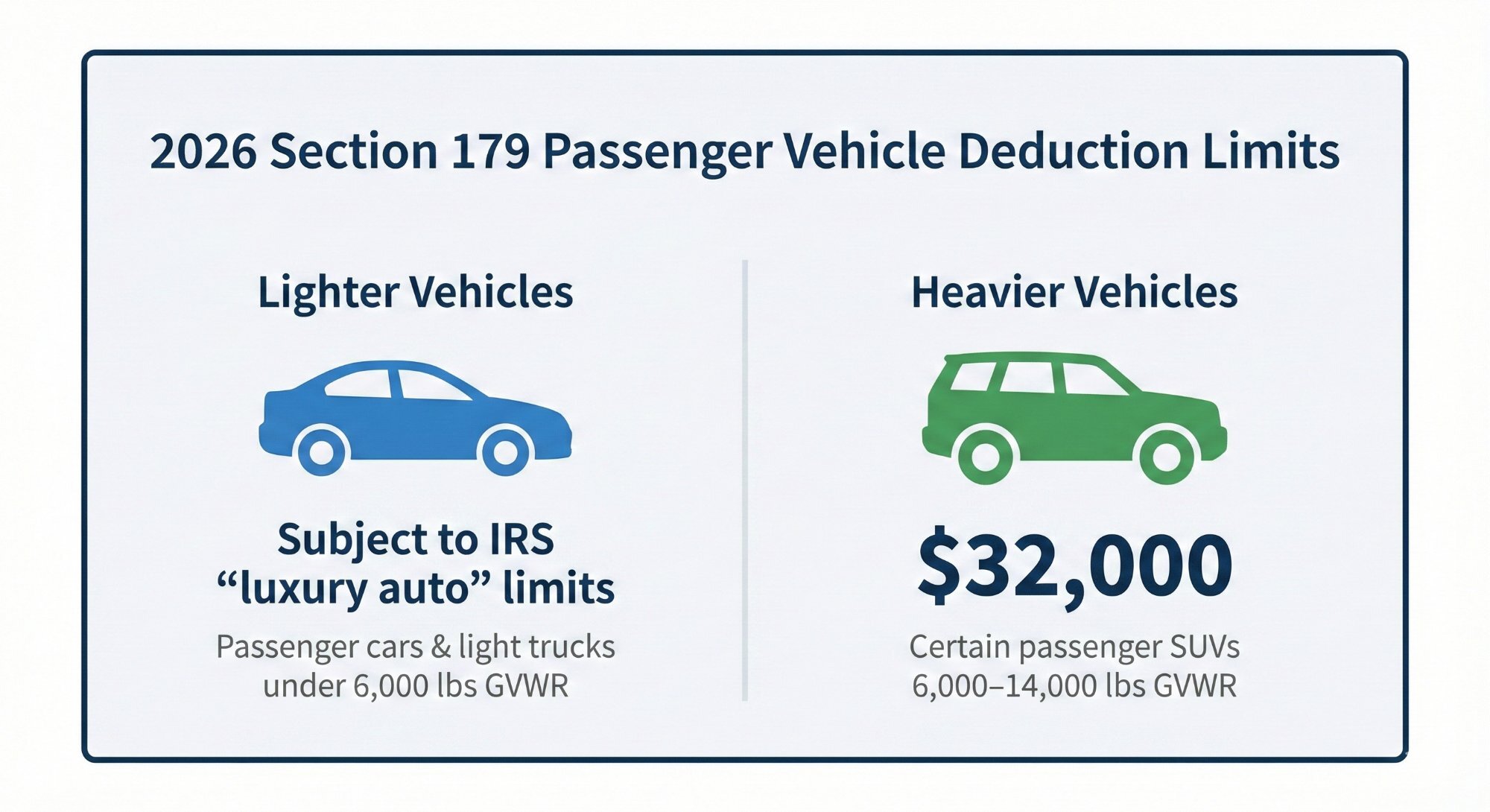

- Certain passenger SUVs have a special $32,000 Section 179 cap for tax years beginning in 2026.

- Passenger cars (and many light trucks/vans) are also subject to IRS “luxury auto” depreciation limits (Section 280F).

- “Placed in service” by year-end is what matters—not when the vehicle is ordered.

Below, we break down vehicle categories, business-use requirements, and compliance best practices. Looking for non-vehicle equipment? See our Qualifying Property guide.

2026 Section 179 Vehicle Deductions At-a-Glance

New & Used Work Trucks and Vans:

May qualify for a large first-year deduction (subject to vehicle type, business-use %, and overall Section 179 limits)

Certain Passenger SUVs (6,000–14,000 lbs GVWR):

$32,000 maximum Section 179 (some pickups/vans are excluded)

Passenger Cars & Light Trucks (Under 6,000 lbs GVWR):

Subject to IRS “luxury auto” depreciation limits (Section 280F)

Placed-in-Service Deadline:

Must be in service by the end of your tax year

Additional Bonus Depreciation:

100% for qualified property acquired and placed in service after January 19, 2025 (subject to eligibility).

How Overall Section 179 Limits Apply to Vehicles (2026)

For tax years beginning in 2026, the maximum Section 179 election is $2,560,000 and begins phasing out dollar-for-dollar when total qualifying property placed in service exceeds $4,090,000. The full phase-out point is $6,650,000.

These overall limits apply to vehicle deductions too—especially for fleets and high-spend years. Vehicle-specific rules (including the $32,000 SUV cap and the luxury auto limits under Section 280F) can still apply even when you’re under the annual Section 179 limit. For full rules and examples, see our Section 179 Deduction (2026) guide.

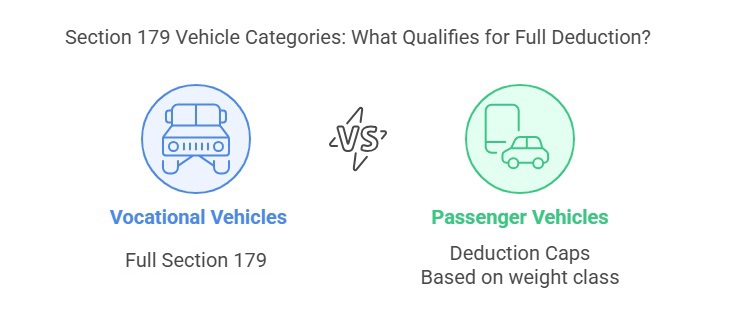

Three Vehicle Categories Under Section 179

Quick GVWR note: GVWR (gross vehicle weight rating) is the manufacturer’s maximum loaded weight rating—check the label inside the driver’s door or the vehicle specs.

1. Vocational/Specialized Vehicles (Any Weight) or Over 14,000 lb. (Full Deduction)

These vehicles generally have little to no personal-use function and are often treated as commercial or “qualified nonpersonal use” vehicles. They may qualify for the full deduction under Section 179 and/or bonus depreciation—subject to the overall Section 179 limits, taxable-income limits, and >50% business-use rules. Keep purchase/financing paperwork, registration/title documentation, and (when applicable) usage records.

Qualifying examples include:

- Heavy trucks over 14,000 lb. GVWR used in construction or hauling

- Specialty work vehicles (cement mixer trucks, garbage trucks, bucket trucks, refrigerated delivery trucks)

- Vehicles seating more than 9 persons behind the driver’s seat

- Delivery trucks with minimal passenger seating

- Cargo vans with permanent commercial modifications (e.g., enclosed cargo area, no seating behind driver)

- Tractors and special‑purpose farm vehicles

- Special‑purpose vehicles like ambulances and hearses

Example: A business purchasing a $120,000 commercial truck (>14,000 lb. GVWR) can potentially deduct the entire amount in 2026, assuming >50% business use and staying within overall Section 179 limits.

2. Heavier Passenger Vehicles (6,000–14,000 lb. GVWR)

Certain passenger SUVs in this weight class have a special $32,000 Section 179 cap for tax years beginning in 2026. Any remaining eligible basis may qualify for bonus depreciation if the vehicle otherwise qualifies and you meet the rules.

The $32,000 SUV cap generally does NOT apply to vehicles that are:

- Designed to seat more than 9 persons behind the driver’s seat

- Equipped with a cargo area of at least 6 feet in interior length that isn’t readily accessible from the passenger compartment

- Vehicles with a fully enclosed driver compartment, no seating behind the driver, and a separate cargo area (certain vans/trucks)

Example Calculation:

- Vehicle Cost: $75,000 SUV (>6,000 lb.)

- Section 179 Deduction (2026 SUV cap): $32,000

- Remaining basis: $43,000 (may be eligible for bonus depreciation if qualified).

- Total First‑Year Deduction: Section 179 deduction plus any applicable bonus depreciation.

3. Cars & Light Trucks (Under 6,000 lb. GVWR)

Passenger cars (and many light trucks/vans under 6,000 lbs GVWR) are subject to IRS “luxury auto” depreciation limits under Section 280F. These limits cap your combined depreciation + Section 179 + bonus depreciation for the vehicle, and the allowed amount is reduced when business use is less than 100%. For the latest IRS passenger-vehicle limitation tables, see the Instructions for Form 4562 and IRS Publication 463.

Business‑Use Requirements & Deadlines

To qualify for Section 179:

- Over 50% Business Use: Exactly 50% doesn’t qualify. Track detailed mileage or usage logs if there’s any chance of personal use.

- Taxable Income Limitation: Keep in mind that your Section 179 deduction cannot exceed your business income in the same tax year. Any unused deduction generally carries forward to future years.

- Ownership & Title: Title the vehicle in your company’s name.

- Placed-in-Service Date: Must be purchased (or financed) and placed in service by the end of your tax year.

- Maintaining Usage: Vehicle business use should remain above 50% over its class life (generally 5 years) or recapture rules may apply.

Important Notes:

- New & Used Vehicles: Section 179 applies to both new and used vehicles—provided they’re “new to you” and purchased in an arms‑length transaction.

- Recapture Risk: If business use drops below 50% in future years—or if you sell the vehicle prematurely—the IRS may “recapture” part of your deduction.

- State Variations: Some states do not fully conform to federal Section 179 rules. See Section 179 by State for details.

- Class Life Tracking: Vehicles typically have a 5‑year class life for tax purposes; maintain usage records throughout this period.

Section 179 Qualified Financing Benefits

Section 179 does not require an upfront cash payment. Both purchases and non-tax capital leases can qualify because the transaction is treated as a purchase for tax purposes. Operating leases typically don’t qualify because you’re generally not treated as the tax owner. Financing allows you to:

- Claim the eligible deduction for the year the vehicle is placed in service (2026 for vehicles placed in service in 2026)

- Spread payments over multiple years

- Improve cash flow while gaining immediate tax savings

Visit our Section 179 Qualified Financing page to explore lender options with Section 179 requirement expertise.

Real‑World Success Story

Example (illustrative): A landscaping company put a used 14,000+ lb. GVWR work truck into service and used it 90% for business:

- Vehicle Cost: $50,000 used work truck (14,000+ lb. GVWR)

- Business Use: 90%

- Potential Section 179 Deduction: $45,000 (90% business use)

- Bonus Depreciation: May also be available depending on eligibility/elections

- Estimated Federal Tax Savings: About $10,800 at a 24% marginal rate (illustrative; actual results vary)

Assumes sufficient taxable income to use the election; state treatment can differ.

This substantial tax benefit helped offset purchase costs while providing essential business equipment for business growth.

Historic Context: The “Hummer Loophole”

Large SUVs once qualified for unlimited write-offs under the so-called “Hummer Tax Loophole,” but the IRS has since placed specific caps on heavy passenger vehicles. However, true commercial vehicles still qualify for full Section 179 deductions, offering significant tax benefits to businesses that require specialized vehicles.

Common Pitfalls to Avoid

- Overstating Business Use – Don’t claim 100% if you occasionally run personal errands. Maintain accurate and detailed logs.

- Misunderstanding SUV Rules – Simply exceeding 6,000 lb. GVWR does not guarantee full deductions for passenger‑type vehicles.

- Not Titling the Vehicle in Business Name – Failing to title in your business name can complicate IRS compliance.

- Missing Deadlines – Ensure the vehicle is placed in service by the end of your tax year (December 31, 2026 for calendar-year taxpayers).

- Ignoring State Rules – Some states do not fully conform to federal Section 179 and/or bonus depreciation. See Section 179 by State

Vehicle Deduction FAQs (2026)

Q: Does a used vehicle qualify for Section 179?

A: Yes—new or used vehicles can qualify if they’re “new to you,” purchased in an arm’s-length transaction, and used more than 50% for business.

Q: Do I have to pay cash to claim the deduction?

A: No. Cash purchases and many financed purchases can qualify if you’re treated as the tax owner and the vehicle meets IRS rules.

Q: What does “placed in service” mean?

A: It means the vehicle is ready and available for business use (not just ordered). It must be placed in service by the end of your tax year.

Q: Does the $32,000 cap apply to all trucks over 6,000 lbs?

A: No. The $32,000 cap applies to certain passenger SUVs. Some vehicles are excluded based on seating/cargo design.

Q: Can I use both Section 179 and bonus depreciation on the same vehicle?

A: Often yes. Section 179 is typically applied first (including any SUV cap), then bonus depreciation may apply to remaining eligible basis if you meet the rules.

Q: What if business use drops to 50% or less later?

A: Recapture rules may apply. Keep mileage/usage logs and review with your tax professional.

Q: Do states follow the same rules?

A: Not always. Some states limit or decouple from federal Section 179 and/or bonus depreciation. See Section 179 by State.

Tools & Resources

Make the most of Section 179 with these tools:

- 2026 Section 179 Calculator

- How to Apply for Section 179 (Form 4562 Election)

- Section 179 vs. Bonus Depreciation

- Section 179 by State (state conformity rules)

- Section 179 Qualified Financing

Professional Guidance: While we strive to provide accurate information, tax regulations are complex and change frequently. Consult a qualified tax professional to:

- Verify qualification requirements

- Optimize deduction strategies

- Ensure ongoing compliance

Additional Resources:

- Instructions for Form 4562: (SUV cap definition + passenger vehicle limitation tables)

- IRS Publication 463: Travel, Gift, and Car Expenses

- IRS Publication 946: How to Depreciate Property

- Rev. Proc. 2025-32: 2026 Section 179 limits (inflation-adjusted)

- Notice 2026-11: bonus depreciation guidance

- Disclaimer:* Section179.Org provides independent research and information but is not affiliated with the IRS. This guide is for general information only and should not replace professional tax advice.*