Updated: January 2026

What “Section 179 Qualified Financing” Means

Definition: “Section 179 Qualified Financing” is an industry term for equipment financing structured so your business is treated as the purchaser (the tax owner) of the equipment—meaning you may be able to claim a Section 179 deduction in the year the asset is placed in service, even though you repay the lender over time.

Key takeaways (2026)

- Financing doesn’t automatically block Section 179: You may be able to claim the deduction even if you finance 100% of the purchase price.

- Placed-in-service timing matters: The asset generally must be delivered and ready for business use within the tax year.

- Business use requirement: The asset must be used predominantly (more than 50%) for business. If business use later drops to 50% or less, IRS recapture rules may apply.

- Loan vs. lease can change the result: Some leases are treated like purchases; others are not. Confirm tax treatment before assuming Section 179 applies.

- Limits still apply: Financing doesn’t override Section 179 caps, phase-outs, or the taxable income limitation.

General information only; consult a qualified tax professional to confirm eligibility for your specific transaction.

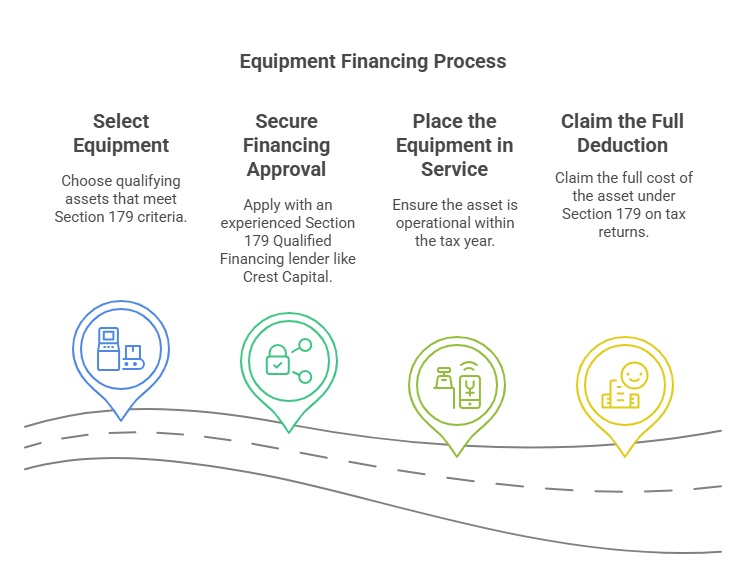

How Section 179 Qualified Financing Works

When you finance your equipment purchase, you can still take full advantage of the Section 179 deduction as long as the asset is placed in service during the tax year. The process is as follows:

This step-by-step flow is designed to help you capture potential tax benefits while financing the purchase over time.

Financing vs. Leasing: What Usually Matters for Section 179

- You must be treated as the owner:

Loans and many “$1 buyout” / finance-lease structures are commonly treated as purchases, while operating leases generally are not. - You must place the asset in service:

Signing paperwork isn’t enough—equipment generally must be delivered and ready for business use within the tax year. - Section 179 rules still apply:

The election can be limited by taxable income and reduced at higher levels of qualifying purchases.

Advantages of Financing and Section 179:

When financing is structured so you’re the tax owner, you may be able to deduct all or part of the equipment cost under Section 179 in the year it’s placed in service—even though you’ll make payments over time. This can improve after-tax cash flow. (You are reading this correctly; in many cases, the tax savings from the deduction will actually leave your bank account healthier than if you had paid cash.) Confirm eligibility and timing with your tax professional.

Eligibility & Credit Requirements

General Section 179 Requirements

- Qualifying Equipment:

The asset must meet Section 179 criteria (e.g., machinery, office equipment, off‑the‑shelf software) and be used more than 50% for business purposes. - Placement in Service:

The equipment must be placed in service during the current tax year.

Section 179 Qualified Financing: Credit Requirements

Crest Capital is one financing option Section179.Org features for businesses looking to preserve cash flow while acquiring qualifying equipment.

What lenders typically look for:

- 2+ years in business under consistent ownership

- Business credit: D&B PAYDEX® of 80+

- Owner credit: 650+ FICO with clean history

- No delinquent accounts

- Prior equipment or vehicle financing, paid as agreed

- Bank statements showing at least $10k in monthly deposits

- Profitable business (also required to fully benefit from Section 179)

These are general benchmarks—requirements vary by transaction. See Crest Capital’s full credit requirements →

Meeting these guidelines doesn’t guarantee approval—final decisions depend on the lender’s full underwriting review.

Real‑World Comparison: Cash Purchase vs. Financed Purchase

Below is a table comparison of the cash flow impact of a cash purchase versus a financed purchase:

|

Factor |

Cash Purchase |

Financed Purchase |

|---|---|---|

|

Initial Cost |

100% upfront |

0%-20% down payment |

|

Immediate Tax Deduction |

Full Section 179 deduction |

Full Section 179 deduction |

|

Working Capital |

Large reduction |

Minimal impact |

|

Flexibility |

Limited by high upfront cost |

Improved liquidity for growth |

This comparison demonstrates that while a cash purchase can deplete available funds, financing allows your business to maintain healthy cash reserves and continue investing in growth.

Financing Considerations for Vehicles

Section 179 vehicle deductions and financing options vary based on three main categories:

Vocational/Specialized Vehicles (Fully Deductible Vehicles):

Work-specific vehicles like heavy trucks, buses, ambulances, and other vehicles that generally have no personal-use function may qualify for more favorable Section 179 treatment. For well-qualified applicants, Crest Capital offers Section 179 Qualified Financing solutions exclusively for these fully deductible vehicles.

Heavier Passenger Vehicles:

SUVs, trucks, and vans in this weight class are subject to specific deduction limits and annual caps. While financing may be available, significant limitations and restrictions apply.

Cars & Light Trucks:

Standard passenger vehicles face strict first-year depreciation limits, so the Section 179 benefit is often limited and standard passenger vehicles are not eligible for Section 179 Qualified Financing.

For current vehicle deduction limits and qualification details, visit our Section 179 Vehicle Deductions (2026 Update) page.

Frequently Asked Questions (FAQs)

Q: Can I claim Section 179 if I finance equipment or vehicles?

A: Yes—if the asset is eligible Section 179 property, placed in service during the tax year, and used predominantly (more than 50%) for business, and Section 179 Qualified Financing is obtained. Annual limits and the taxable income limitation still apply. For 2026 limits, see Section 179 Deduction (2026).

Q: Do I have to pay off the loan to claim Section 179?

A: Generally, no. The election is tied to ownership and placed-in-service timing—not how much cash you’ve paid so far. Confirm the structure with your lender and tax professional.

Q: Does a lease qualify the same way as a loan?

A: Not always. In general, you must be treated as the owner for tax purposes to claim Section 179. Many finance-lease structures (including $1 buyout structures) may qualify, while operating leases generally do not. Confirm treatment with your tax professional.

Q: What does “placed in service” mean?

A: It generally means the asset is delivered and ready for its intended business use during the tax year.

Q: What if my business has low taxable income this year?

A: Section 179 is generally limited by taxable income, and any unused amount may carry forward. You may also want to compare Section 179 vs. bonus depreciation.

Q: What are the key credit requirements for Section 179 Qualified Financing?

A: Underwriting varies by lender, but common factors include time in business, business credit, owner credit (for closely held companies), and financial strength. The “Eligibility & Credit Requirements” section above summarizes typical Crest Capital benchmarks.

For additional questions, please visit our Section 179 FAQs page.

Next Steps & Call-to-Action

Ready to Optimize Your Equipment Purchase?

- Calculate Your Savings:

Use our Section 179 Calculator to estimate your tax savings with a financing scenario. - Contact a Financing Specialist:

For personalized advice, reach out directly to Crest Capital at (800) 245-1213 or apply online to explore flexible financing options tailored to your business needs.

If financing fits your business, take advantage of Section 179 Qualified Financing today to maximize your tax benefits and secure the equipment your business needs without compromising cash flow—subject to eligibility, timing, and the structure of the transaction.

Related Topics & Additional Resources

For IRS guidance on depreciation and Section 179, see IRS Publication 946 and Instructions for Form 4562. For rules on determining an asset’s cost basis (including financed amounts), see IRS Publication 551.

Section179.Org is an independent educational resource. This content is for general informational purposes only and is not tax, legal, or financial advice. Consult a qualified tax professional regarding your specific situation.