What Is the Difference Between Section 179 and Bonus Depreciation?

Section 179 and bonus depreciation both accelerate first‑year deductions, but they differ in dollar limits, elections, and how they interact with business income. For tax years beginning in 2026, Section 179 provides targeted control up to the $2,560,000 limit (subject to the taxable income limit and phase‑out rules), while bonus depreciation can provide an uncapped deduction and may create or increase a net operating loss. Many businesses coordinate the two by electing Section 179 on priority assets first, then applying bonus depreciation to any remaining eligible basis.

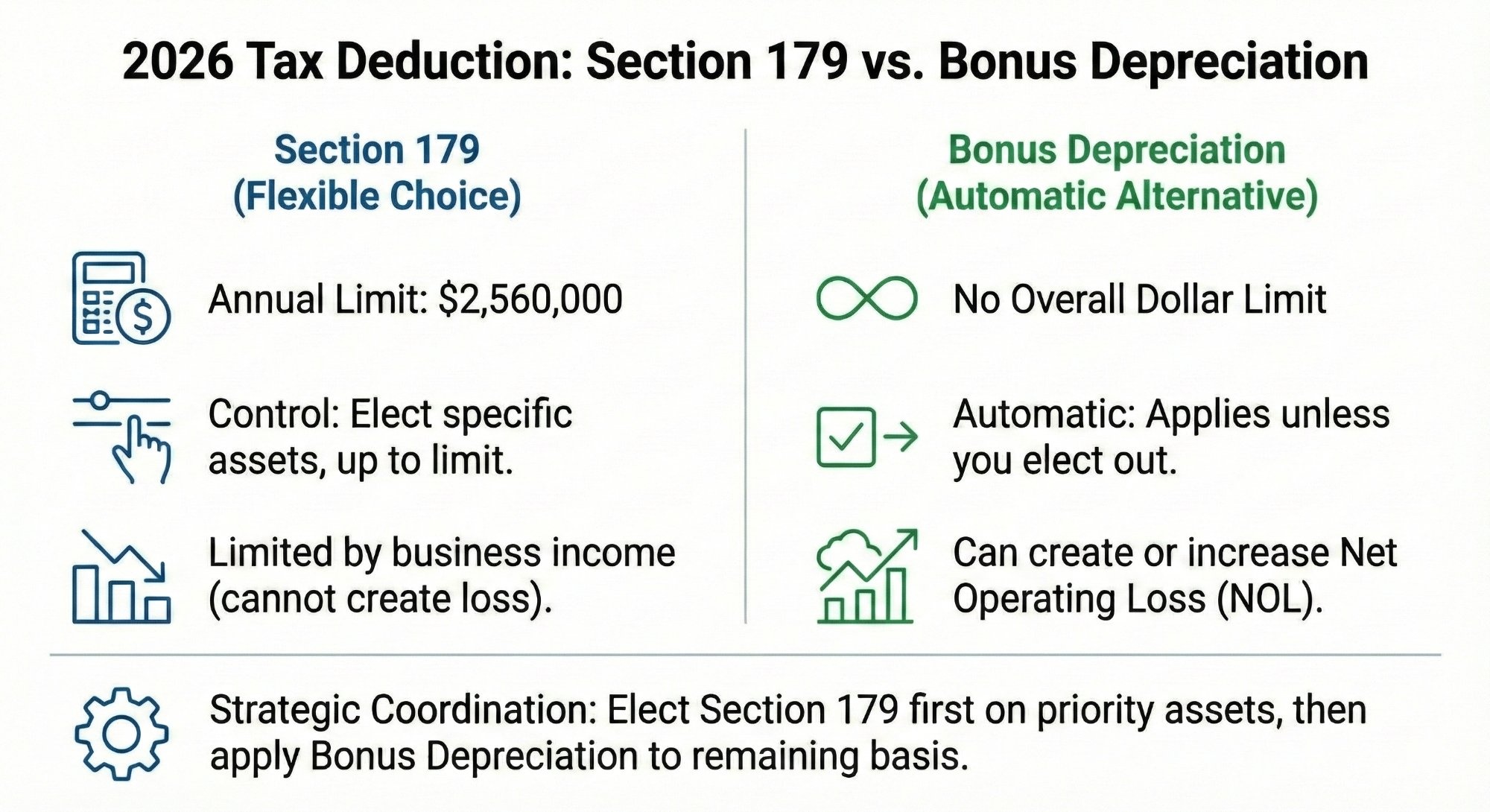

Section 179 vs Bonus Depreciation: Key Differences for 2026

Business owners and tax professionals know that choosing the right way to recover equipment and software costs can affect taxable income and cash flow.

Definitions:

- Section 179 deduction: An election to expense some or all of the cost of qualifying business property in the year it’s placed in service (subject to annual dollar limits and a taxable income limitation).

- Bonus depreciation: An additional first‑year depreciation deduction under Section 168(k) that generally applies automatically to eligible property unless you elect out.

This guide explains how to choose—and how businesses often coordinate both tools: elect Section 179 first on priority assets, then apply bonus depreciation to any remaining eligible basis.

2026 Snapshot (Federal)

- Section 179 Maximum Deduction: $2,560,000 (tax years beginning in 2026)

- Phase‑out Begins Above: $4,090,000 of total qualifying property placed in service

- Full Phase‑out: $6,650,000

- Bonus Depreciation: Generally 100% for qualified property acquired and placed in service after Jan. 19, 2025

- Income Rules: Section 179 is limited by business taxable income; bonus depreciation can create or increase a net operating loss

Note: General information only. Confirm eligibility, timing, and any business-income limits with your tax professional.

Updated June 10, 2026. Figures reflect 2026 tax-year limits — confirm with IRS guidance or your tax professional.

Key Differences at a Glance (2026)

- Deduction Limits:

- Section 179: Has a defined maximum deduction ($2,560,000 for tax years beginning in 2026) and a phase‑out threshold ($4,090,000) that reduces the deduction dollar‑for‑dollar when exceeded.

- Bonus Depreciation: No overall dollar limit; generally 100% for qualified property acquired and placed in service after Jan. 19, 2025.

- Timing & Phase‑Down:

- Section 179: A permanent part of the tax code with annual inflation adjustments.

- Bonus Depreciation: Generally 100% for qualified property acquired and placed in service after Jan. 19, 2025 (rules vary by property type and elections).

- Income Limitations:

- Section 179: Limited by your business’s taxable income (cannot create a loss).

- Bonus Depreciation: Can create or increase a net operating loss, offering additional flexibility.

Understanding Section 179: The Flexible First Choice

Overview:

Section 179 lets a business elect to expense (deduct immediately) all or part of the cost of qualifying assets—such as machinery, vehicles, or software—in the year it is placed in service, rather than depreciating it over multiple years.

Core Benefits:

- Control: You choose which assets (and how much of each) to expense.

- Planning tool: Useful for targeting a specific taxable income level.

- Vehicles & software: Certain vehicles and software can qualify—see the Section 179 Vehicle and Section 179 Software pages for details.

Current Limitations (Tax Years Beginning in 2026):

- Maximum deduction: $2,560,000

- Phase‑out threshold: $4,090,000 (dollar‑for‑dollar reduction above this amount)

- Full phase‑out: $6,650,000

- Deduction cannot exceed business taxable income (unused amounts can generally be carried forward)

Note: The Section 179 deduction phases out dollar‑for‑dollar when the total cost of qualifying property placed in service exceeds $4,090,000 and is fully phased out at $6,650,000.

These dollar limits are adjusted annually for inflation. For background on recent rule changes and effective dates, see the Legislative History page.

Example: A business places $800,000 of equipment in service in 2026. If it has sufficient taxable income, it can elect to expense the full $800,000 under Section 179.

Understanding Bonus Depreciation: The Automatic Alternative (2026)

Overview:

Bonus depreciation (the “additional first-year depreciation deduction”) generally applies automatically to eligible property and accelerates depreciation into the first year. Under current law, the bonus rate is generally 100% for qualified equipment acquired and placed in service after Jan. 19, 2025.

How It Works:

- Applies to both new and used property with a recovery period of 20 years or less.

- After any Section 179 election, bonus depreciation generally applies automatically to the remaining eligible basis unless you elect out for the relevant class of property.

- Electing out is typically an all-or-nothing election by class of property, not item-by-item.

Bonus Depreciation: Generally 100% for Qualified Property Acquired After Jan. 19, 2025:

- Current law generally provides a 100% additional first‑year depreciation deduction for qualified property acquired and placed in service after Jan. 19, 2025. IRS Notice 2026‑11 provides interim guidance. See our Legislative History page for background.

Note for certain fiscal-year taxpayers: A special election under §168(k)(10) may allow a 40% rate (60% for certain longer-production property) for qualified property placed in service during the first taxable year ending after Jan. 19, 2025. This election is narrow and fact-specific—consult your tax advisor.

- Coordination with Section 179: Section 179 expensing is elective on an asset‑by‑asset basis (you select specific items to expense up to the $2,560,000 annual limit), while bonus depreciation generally applies automatically to eligible property unless you elect out (by class of property). Understanding this distinction helps you coordinate both tools for tax planning. For more on the Section 179 election, see How to Apply (Section 179 Election).

Key Advantages:

- No overall dollar cap: Useful for large capital expenditures.

- Can create a loss: May generate or increase an NOL (subject to applicable NOL rules).

- Simple default behavior: Often applies automatically unless you elect out.

Use our Section 179 Calculator to model your potential savings »

When to Use Each Strategy

Section 179 is ideal when:

- You want control over which assets get expensed this year.

- Your total qualifying purchases are within Section 179’s annual limits (and below the phase‑out threshold).

- You want to avoid (or limit) creating an NOL.

Bonus Depreciation is advantageous when:

- Your total qualifying purchases exceed the Section 179 phase‑out threshold (so Section 179 is reduced or eliminated).

- You want the largest possible first-year deduction, even if that creates an NOL.

- You prefer the simplicity of the default rules (unless you need to elect out).

Decision Factors to Consider:

- Taxable income now vs later: Do you expect higher income in future years where depreciation deductions might be more valuable?

- Cash flow: A larger first-year deduction can improve after-tax cash flow.

- State tax treatment: Many states do not fully conform to federal bonus depreciation.

- Placed-in-service timing: Deductions are based on when the asset is placed in service, not when ordered or paid for.

- Financing: Financing is fully eligible, and encouraged. See Section 179 Qualified Financing.

Example: A company investing $4,000,000 in equipment might elect to expense $2,560,000 under Section 179 (subject to the taxable income limit) and then apply bonus depreciation on the remaining $1,440,000 (if eligible) to maximize first‑year deductions.

For more on electing these deductions, see Electing Section 179 »

Strategic Integration: Coordinating Both Tools

Many businesses benefit from a hybrid approach:

- Section 179 first: Elect expensing on the highest-priority assets (up to the annual limits).

- Bonus depreciation next: Apply bonus depreciation to remaining eligible basis (unless you elect out).

- MACRS last: Depreciate any remaining basis over the normal recovery period.

Example: In 2026, a company with $3,500,000 in equipment investments might:

- Deduct $2,560,000 under Section 179,

- Claim 100% bonus depreciation on the remaining $940,000 (if eligible),

- No remaining basis for MACRS depreciation.

Special Considerations

State Tax Impact:

- Some states partially conform or fully decouple from federal bonus depreciation.

- Always confirm state treatment before finalizing your strategy. See Section 179 by State for a conformity overview.

Qualified Improvement Property (QIP):

- Section 179: QIP can be eligible for Section 179 when you elect to treat certain qualified real property as section 179 property and the property meets the QIP definition (generally, interior improvements to nonresidential real property placed in service after the building was first placed in service—excludes enlargements, elevators/escalators, and structural framework). See Qualifying Property for details.

- Bonus depreciation: QIP is generally eligible for bonus depreciation when treated as 15-year property and otherwise meets the rules.

- Common pitfalls: Be careful with classifications, placed-in-service dates, and elections that can change depreciation methods for certain real property.

Documentation & Compliance:

Maintain meticulous records to support your deductions:

- Purchase dates, costs, and placed‑in‑service dates

- Business use percentages and asset classifications

- Copies of Form 4562 and related election statements

Planning for the Future

Planning for 2026 and beyond:

- Time your investments: Place qualifying property in service by the end of your tax year to capture current-year deductions.

- Refine your strategy: Coordinate Section 179 with bonus depreciation based on income, cash flow, placed‑in‑service timing, and state conformity.

- Integrate financing: Equipment financing can help you acquire assets now while preserving cash. See Section 179 Qualified Financing.

For comprehensive planning, consulting a tax professional is advised.

Frequently Asked Questions

Q: Can I take both Section 179 and bonus depreciation on the same purchase?

A: Often, yes. Businesses commonly elect Section 179 first to expense priority assets, then apply bonus depreciation to remaining eligible basis (unless they elect out of bonus depreciation for that class of property).

Q: Does Section 179 have a taxable income limit?

A: Yes. Section 179 generally can’t create a loss; unused Section 179 may generally be carried forward. Bonus depreciation can create or increase a net operating loss.

Q: Is bonus depreciation automatic?

A: Generally, yes. Taxpayers can elect out of bonus depreciation for a class of property, so planning matters.

Q: What does “placed in service” mean?

A: Generally, it means the asset is ready and available for its intended business use. Buying or paying for an asset isn’t enough if it isn’t placed in service by the end of your tax year.

Q: Do I have to buy new equipment to qualify?

A: Not necessarily. Section 179 can apply to new or used qualifying property. Bonus depreciation can also apply to used property if it meets eligibility rules (including that it’s new to the taxpayer).

Q: Does qualified improvement property (QIP) qualify?

A: QIP can be eligible for both Section 179 (when you elect to treat certain qualified real property as section 179 property) and bonus depreciation, subject to the specific rules.

Q: Do states follow federal Section 179 and bonus depreciation rules?

A: Not always. State conformity varies and can change—confirm your state treatment before assuming the same result on your state return.

Q: Does financing prevent these deductions?

A: Financing typically doesn’t prevent eligibility by itself; what matters is basis and placed‑in‑service timing. Confirm details with your tax professional.

Conclusion & Recommendations

Section 179 and bonus depreciation are two primary tools for accelerating first‑year deductions. See the direct answer at the top of this page for how they compare for tax years beginning in 2026—and use the Section 179 Calculator to model your own numbers.

Related Section 179 Topics

Sources:

- Rev. Proc. 2025-32 (2026 Section 179 inflation adjustments): https://www.irs.gov/pub/irs-drop/rp-25-32.pdf

- Notice 2026-11 (bonus depreciation guidance): https://www.irs.gov/pub/irs-drop/n-26-11.pdf

- Instructions for Form 4562: https://www.irs.gov/instructions/i4562

For the IRS’s general guidance on depreciation and the Section 179 deduction, see IRS Publication 946, How To Depreciate Property and About Form 4562.

Disclaimer: The content on this page is intended solely for general informational and educational purposes and does not constitute professional tax, legal, or financial advice. Although Section179.Org believes the information provided is accurate, tax laws, regulations, and policies are subject to change without notice. The discussion of Section 179, bonus depreciation, and related strategies—including comparisons, examples, and state-specific details—is provided “as is” and may not reflect the most current legal or regulatory developments. Section179.Org, its affiliates, and contributors assume no liability for any errors, omissions, or for any decisions or actions taken in reliance on this information. Users are strongly advised to consult with a qualified tax professional or legal advisor and verify the latest guidance from official sources before making any tax planning or business decisions.